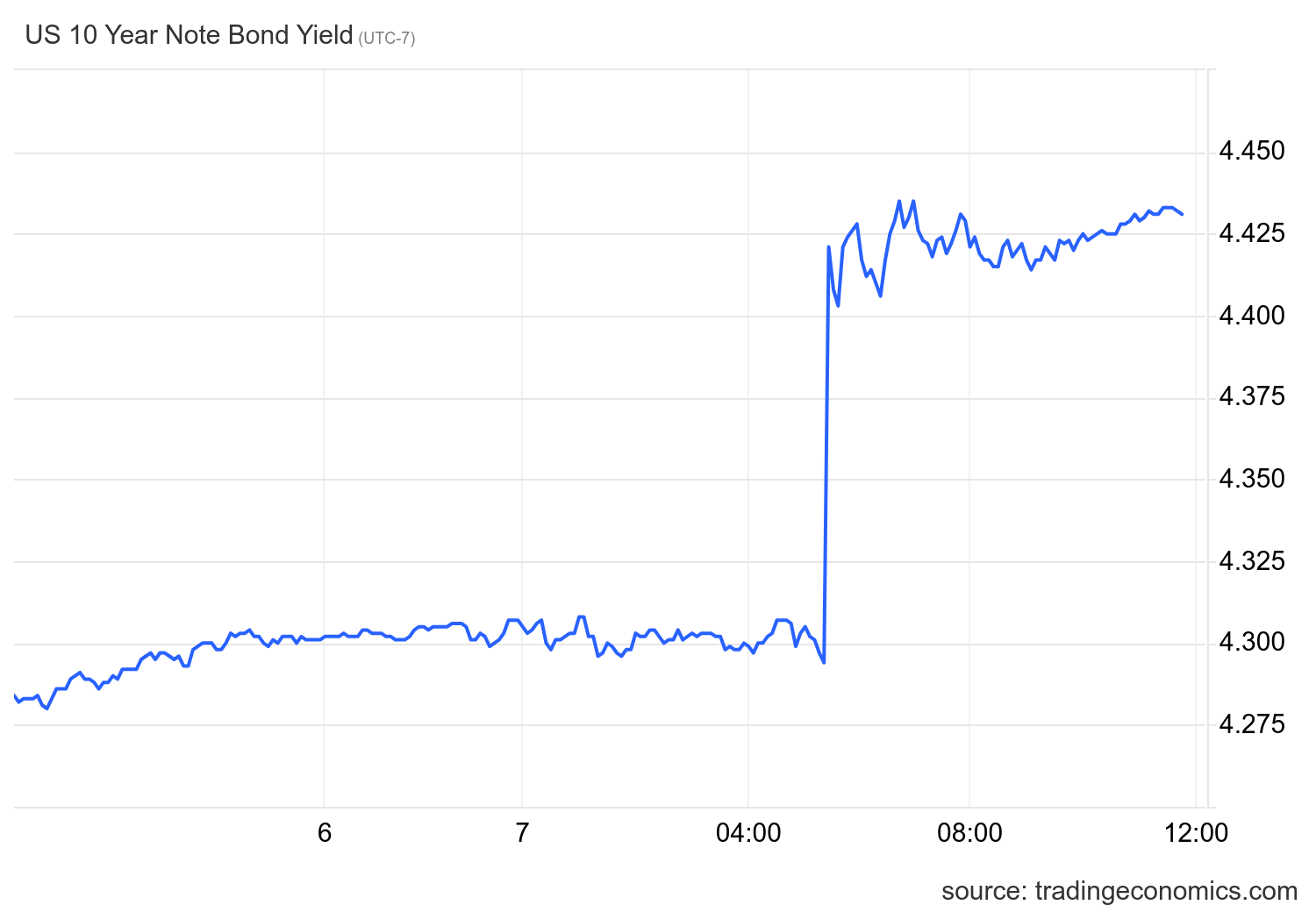

this Bureau of Labor Statistics Employment report shows the honey badger labor market woke up this morning and is choosing violence again. Not only did the overall employment data beat expectations, but the negative revisions were also small and wage growth accelerated. This was clearly negative for mortgage rates as bond yields were close to breaking through key technical levels, but the trend reversed.

Fortunately for the mortgage industry United States Federal Reserve focuses more on the underlying data it tracks rather than the headlines printed by the Bureau of Labor Statistics. When asked at a recent meeting whether strong overall employment data would lead to a rate hike, Fed Chairman Powell responded that inflation is falling faster than expected and the labor market will create a lot of jobs in 2023. . Jobs Week takes a more nuanced view, and one jobs report isn’t the only basis for its decisions. Let’s review what the Fed is watching.

Job vacancy data

The Fed likes job openings data because they see it as a precursor to an imbalance in the labor supply. My working theory is that the Fed wants to see us get down to 7 million job openings — then they will adopt a more dovish tone. We’ve come down from the record 12 million Post-COVID vacancies approaching 800w. Weak labor data makes the Fed smile, but we’re not there yet.

The exit rate (the key data line I use to show whether the labor market is tight) is back to pre-COVID-19 levels. According to the Fed’s tracking, we are no longer in a tight labor market. However, I believe 7 mega The number is their vacancy target level, and when we hit that target, the turnover percentage should drop below 2%.

Number of people applying for unemployment benefits

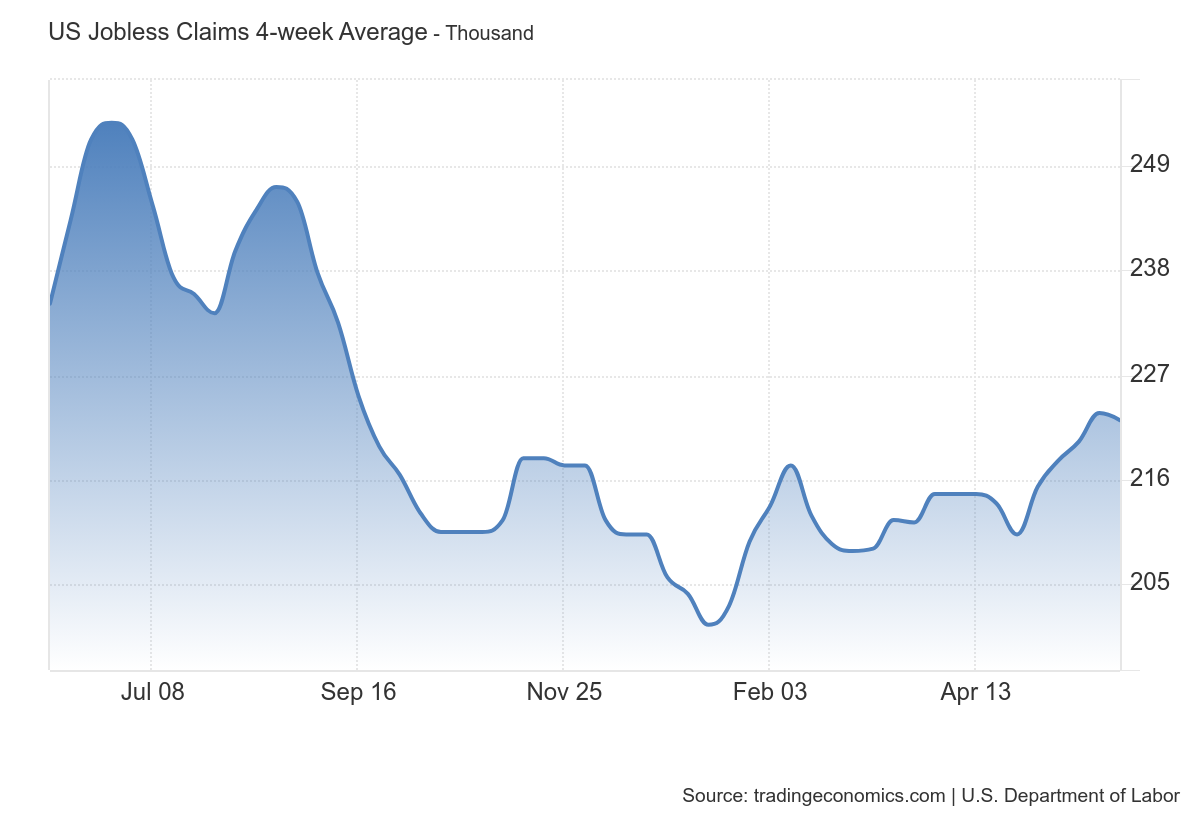

To me, unemployment claims are the key trigger of a labor force recession. My recession target level is the 4-week moving average of 323,000. If the Fed waits to pivot even as we approach or reach this number, the soft landing will disappear. Anything close to that number is a very pessimistic sign for the labor force. Initial jobless claims are up from recent lows, but not enough to warrant the Fed’s attention, and with Jay Powell saying the Fed will be watching the claims data, it’s key to track each week data cable. This week, we saw a modest decline, but it moved higher from the recent lows.

U.S. Bureau of Labor Statistics Friday jobs

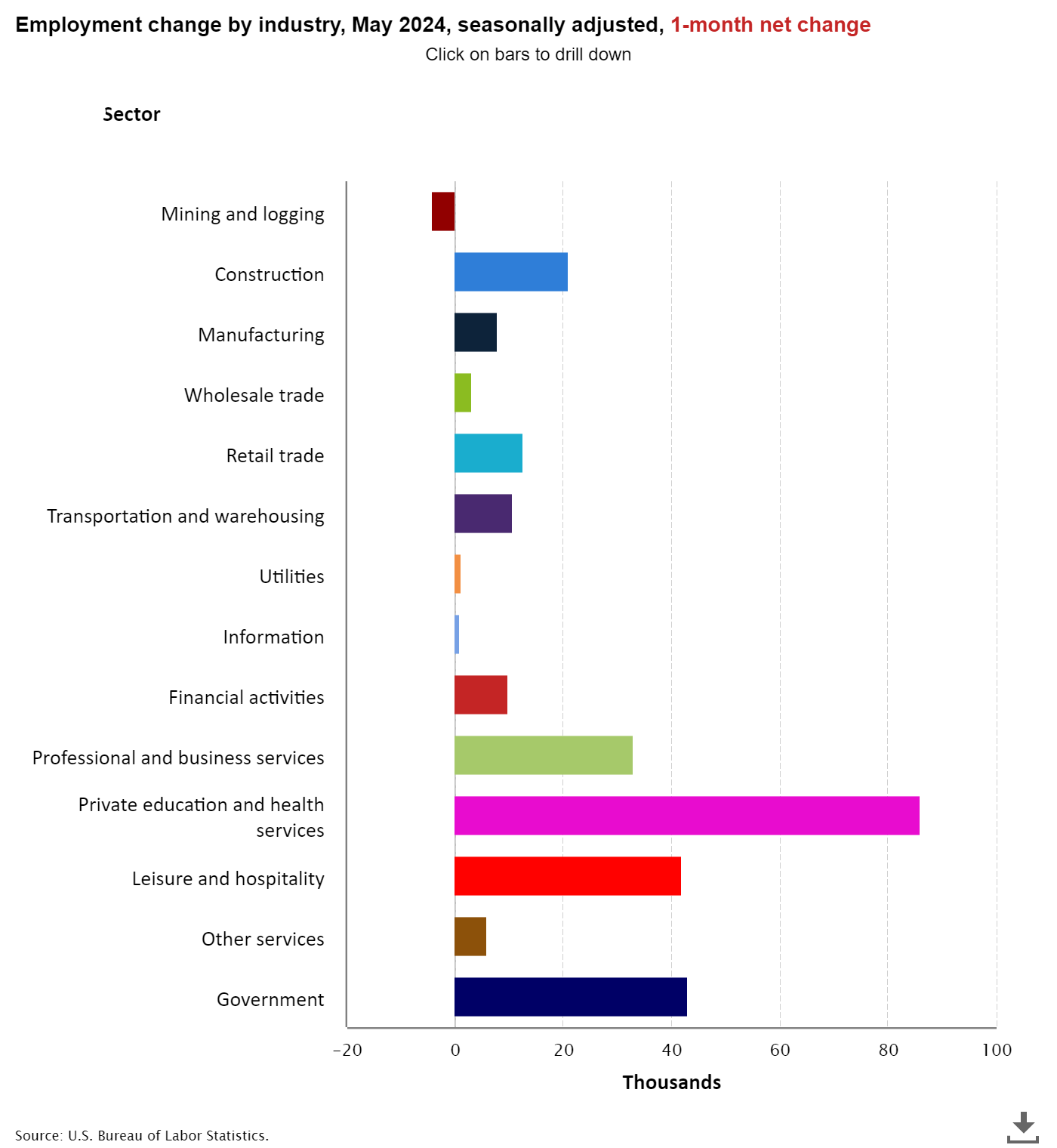

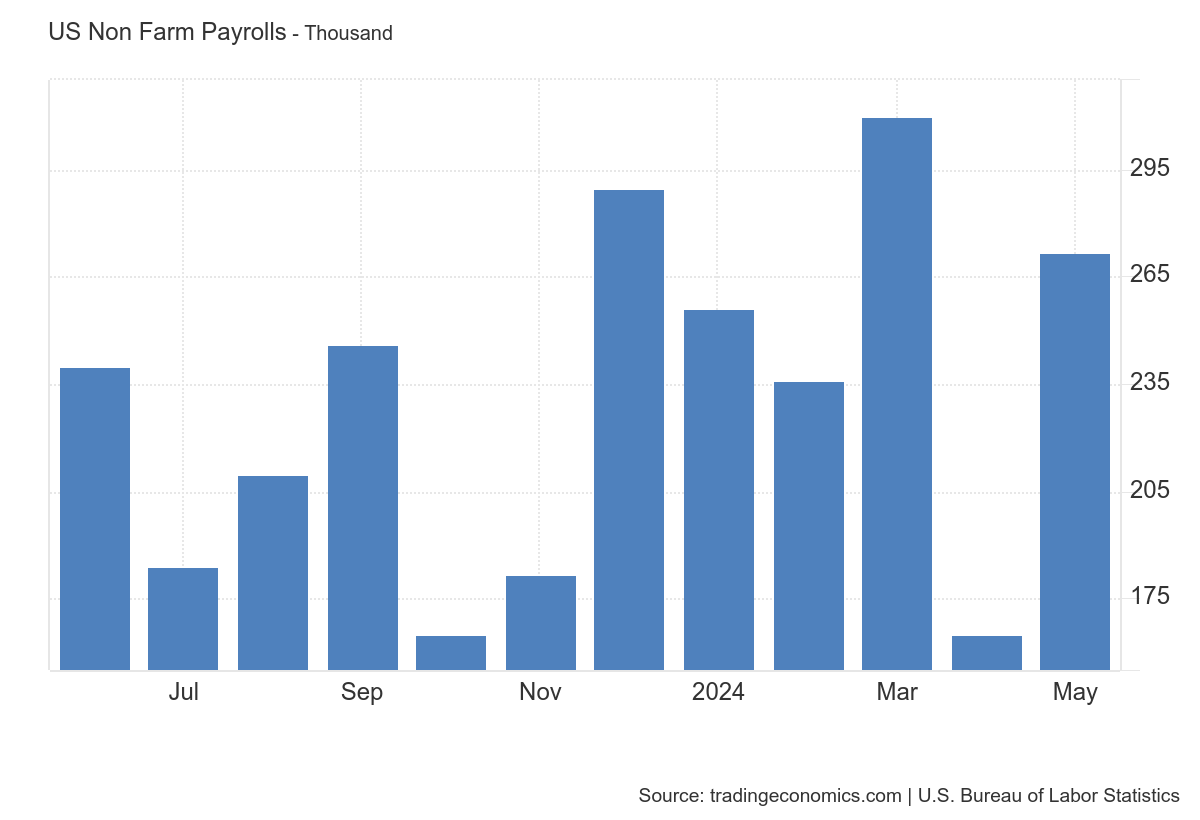

From the Bureau of Labor Statistics: The U.S. Bureau of Labor Statistics reported today that non-agricultural employment increased by 272,000 people in May and the unemployment rate was little changed at 4.0%. Employment continues to trend upward across multiple industries, led by health care; government; leisure and hospitality; and professional, scientific and technical services.

Here are details on the jobs created this month:

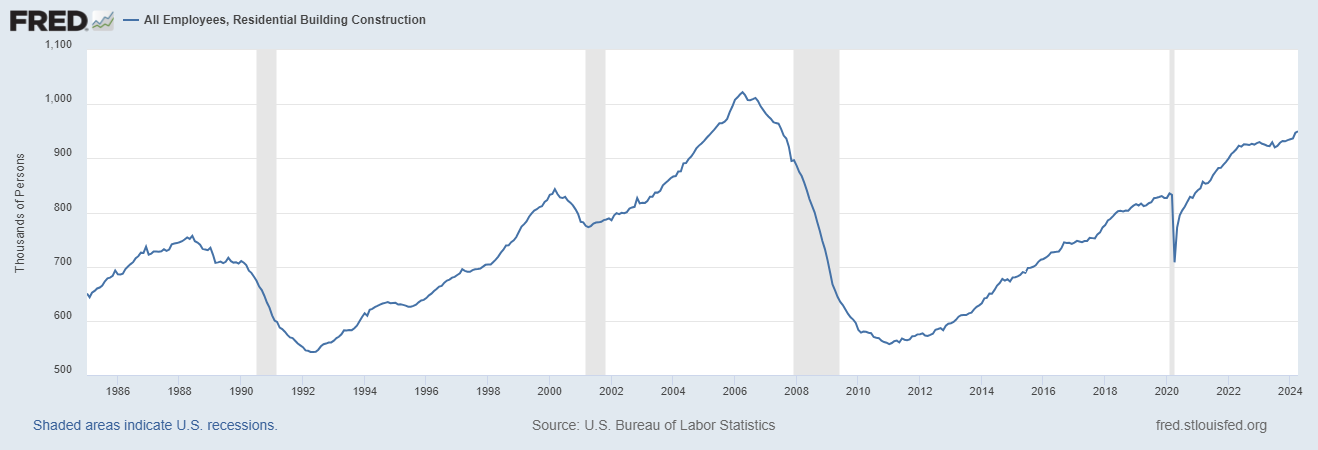

As always, one of the labor sectors I focus on in recessions is residential construction workers, who tend to lose their jobs before recessions. So far, this has not happened. Note: Don’t put all your eggs in the inverse yield curve basket when economic data doesn’t look recessionary. I believe this is the biggest mistake stock traders have made over the past two years.

Wage growth data is critical to me and my Fed model. I believe the Fed’s goal is Salary growth 3% Because they believe the productivity data is not as strong as they report. So, while wage growth is not out of control and has been cooling since 2022, I think we need to get below 3.5% for the final countdown to 3% wage growth, when the Fed becomes less hawkish.

This is a key topic I want to discuss. One of my calls for labor market recovery is based on the premise that if we had not experienced COVID-19, there would be somewhere between 157 million and 159 million people working. As the economic cycle progresses and employment approaches 159 million, job growth numbers should cool. This means our trend should be 140,000 and 165,000 per month as we get closer 159 million Employed Personnel. So far this call doesn’t look good given our current situation Total non-agricultural employment population: 158,543,000 The average for the past three months is 249,000.

However, I do expect the overall employment data to slow down. Since this data line should slow, the unemployment rate should rise over the next 12 months. Unless we add 250,000 jobs a month, keeping the unemployment rate low will be more complex and challenging. This is something to consider for the rest of this year and into 2025.

Overall, the key jobs data beat expectations and wage growth was slightly stronger than expected, but the weekly jobs numbers still show me what I’ve been seeing for months: The labor market is getting softer, but not imploding yet. Labor data has been critical for mortgage rates because I believe the bond market will do a lot of the early heavy lifting for the Fed once we get the labor data, and they won’t mind if mortgage rates go lower.