If we took the worst spread levels from 2023 and combined them to today, mortgage rates would be 0.48% Now higher. While our spreads are far from average, the improvement we’ve seen this year is a plus.

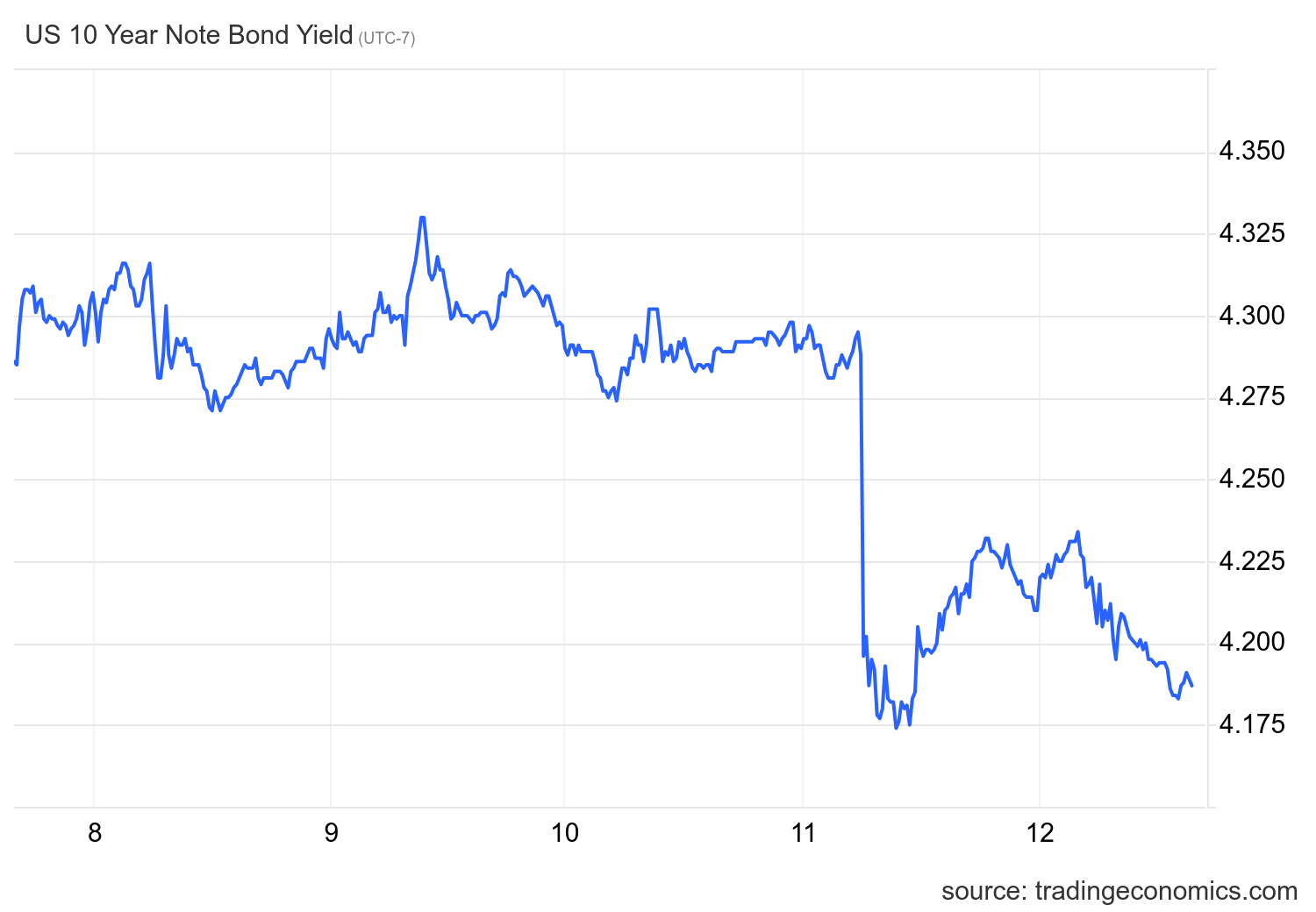

10-Year Yield vs. Mortgage Rates

Last week’s inflation data and testimony United States Federal Reserve The inauguration of President Jerome Powell has been a boon for mortgage rates, as the 10-year Treasury yield fell to the key 4.20% level. This is a tough spot to break out of, so the key this week is to make follow-on bond purchases after a close below 4.20%. If that doesn’t happen soon, we’ll need to wait for more economic data or Fed talking points to push the 10-year yield lower.

Purchase application data

The last time we saw a positive 12-week trend in app shopping was when mortgage rates hit 6%. Buying apps have performed well in four of the last five weeks, while mortgage rates aren’t even 6%. Context is crucial now as we are working from the lowest levels ever, so as the past five weeks have shown, it doesn’t take much to buy apps to push the needle higher.

However, let’s keep an eye on this story over the next six months because the data for late 2022 and 2023 are showing us this: If mortgage rates fall and we get at least two to three months of positive data, Then show up in future existing home sales reports. Keep in mind that purchasing an app will require waiting 30-90 days for the data to appear in sales reports later.

Since mortgage rates began to fall in November 2023, we have seen 16 positive photos, 14 negatives and Two flat prints in weekly data. However, as mortgage rates began to rise earlier this year, we observed a decline in demand. Data so far in 2024 remains unfavorable; 10 positive photos, 14 negatives and two Flat print.

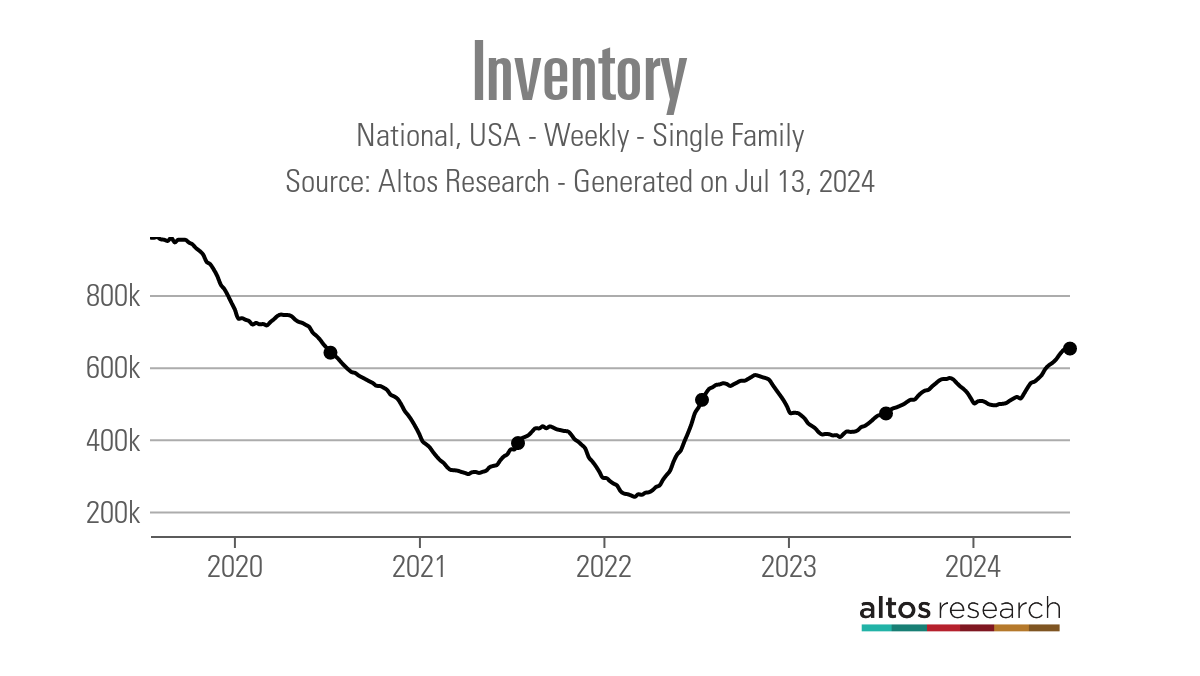

Weekly housing inventory data

This week’s data is affected by the July 4th bug. Especially if the 4th of July falls on a Thursday or Friday, people tend to take longer vacations. So I won’t say anything about the weekly decline in stocks, just the impact of the holidays and the trend should resume next week.

- Weekly inventory changes (July 5-12): Inventory declines 652,573 arrive 651,453

- Same week last year (July 7-14): Inventories rising 466,534 arrive 471,603

- Historical inventory bottom occurs in 2022 240,497

- Annual inventory peak in 2024 is 652,573

- For some purposes, active listings this week in 2015 were 1,197,439

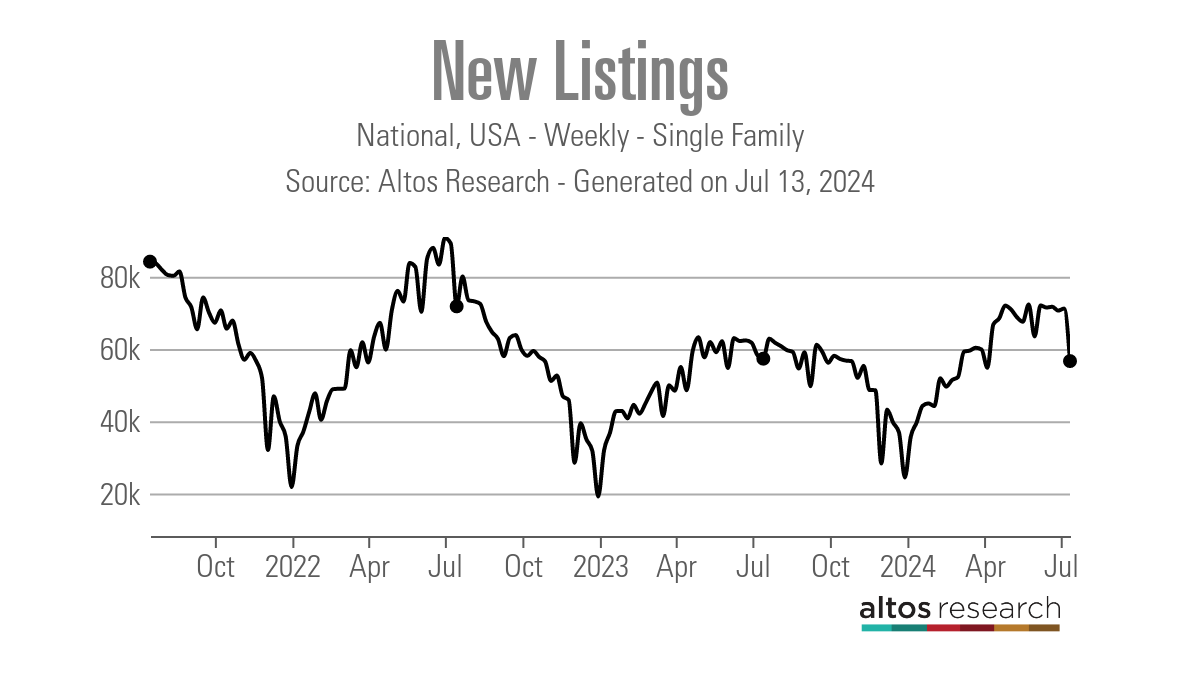

New listing data

The drop in new listings this week was much larger than I expected, but that was the July 4th weekend, so I wouldn’t bet on anything. I’ll be keeping an eye on this over the next few weeks, though. The seasonal decline is about to begin, so we should get used to seeing a decline in new listings towards the end of the year.

I’m a little shocked that new listings this week are even lower than last year: it’s the lowest new listings week ever. Here are the new slates from last week over the past few years:

- 2024: 56,638

- 2023: 57,304

- 2022: 71,790

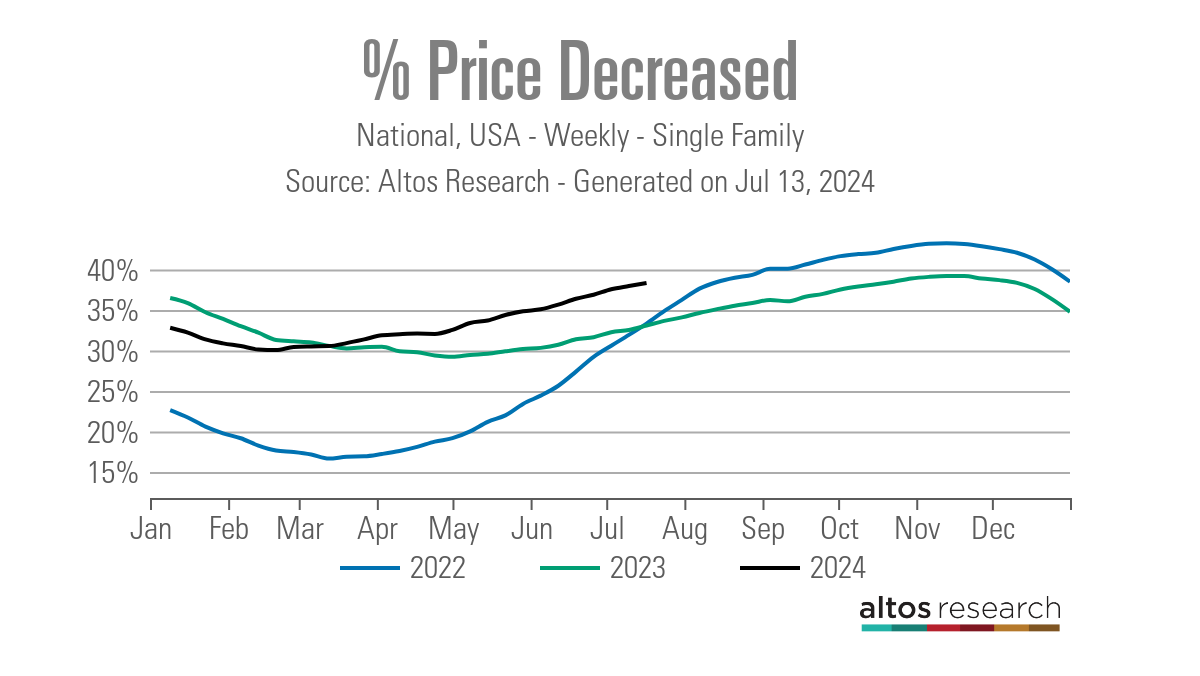

Price reduction percentage

On average, one in three homes loses price every year—standard housing activity. With interest rates remaining high, price reduction percentages are higher than in the past two years, and inventory data in some parts of the country is higher than national data.

A few weeks ago, I discussed on the HousingWire Daily podcast that price growth data would cool down in the second half of the year. Here are last week’s price reduction percentages over the past few years:

- 2024: 38%

- 2023: 33%

- 2022: 33%

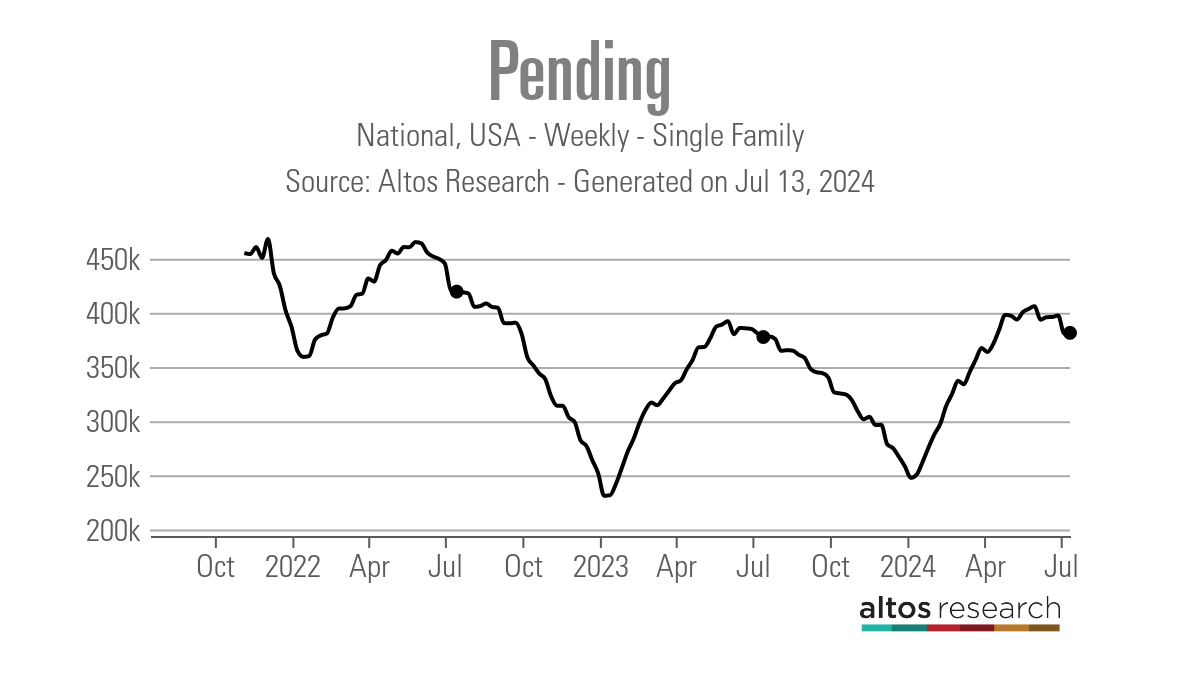

for sale

Below is altos research corp. Weekly open contract data shows immediate demand compared with the same period last year. Our demand has increased this year as more sellers become buyers. These are instant weekly contracts, while purchase application data takes 30-90 days. Our weekly pending sales data relates to contracts.

- 2024: 381,524

- 2023: 377,650

- 2022: 419,524

The week ahead: Powell speaks again, plus retail sales and housing starts

Powell will speak again on Monday, and several Fed chairmen will also speak this week. I’d like to see if there are more dovish statements from other Fed presidents this week. Retail sales data is on Tuesday and housing starts data is on Wednesday. A major focus of the housing starts data will be whether single-family home permits continue to decline, which would be detrimental to the exodus of construction labor. Additionally, we have Thursday’s all-important jobless claims data.