Mortgage rates fell sharply last week while the Federal Reserve held off on cutting rates, largely because the labor market has softened. Can mortgage rates get lower?

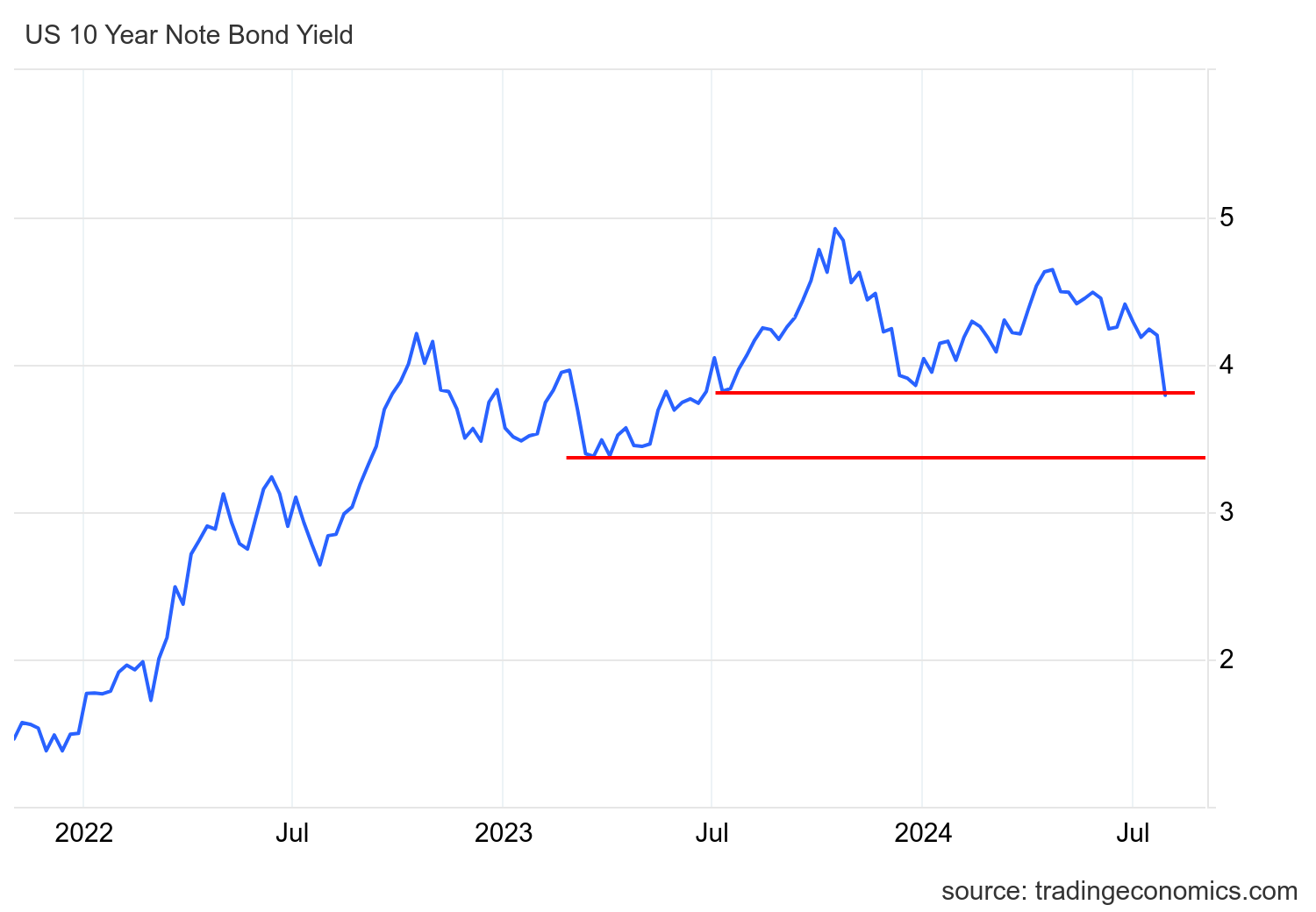

As the chart below shows, when markets priced in economic weakness in early 2024, the 10-year Treasury yield fell to 3.80% but did not breach that level. So, following the weak jobs report, the question is: Can this level break out and fall back to the key line (which I call the Gandalf line at 3.37%)? I write about Friday’s jobs report and discuss all the labor force data we got last week.

10-Year Yield vs. Mortgage Rates

My 2024 predictions include

- Mortgage interest rates range from 7.25%-5.75%

- The 10-year Treasury bond yield is between 4.25% and 3.21%

The 10-year Treasury yield is as high as 4.70% this year as inflation heats up and economic data exceeds expectations at the beginning of the year, but mortgage rates are not moving as closely as last year as mortgage spreads improve in 2024. Labor data has been weak for months. So now we are at a critical point with the 10-year yield around 3.80%.

Since the Fed has yet to adjust or cut interest rates, the bond market needs to shoulder the burden for the Fed, which is deliberately behind the curve. For a clear breakout from here, we need to continue to see weaker data.

mortgage spread

Mortgage spreads a negative storyline in 2023 as Silicon Valley Bank The collapse and resulting banking crisis pushed spreads to new cycle highs. We don’t have that variable this year, and spreads are improving sooner than I thought, which is helping mortgage pricing. We also have a lot of downside in our spreads.

If we took the worst spread levels from 2023 and combined them to today, mortgage rates would be 0.49% Now higher. While our spreads are far from average, the improvement we’ve seen this year is a plus.

Purchase application data

Due to the recent drop in mortgage rates, home purchase application data was flat, with four weeks of positive territory and four weeks of negative territory. However, everyone was shocked when the three consecutive weeks of growth in purchase application data we saw in early June trickled down to the pending home sales data. Remember, we are operating at historically low levels, so it doesn’t take much to change direction. Another negative photo last week.

Since mortgage rates began to fall in November 2023, we have seen 16 positive photos, 17 negatives and Two flat prints in weekly data. However, as mortgage rates began to rise earlier this year, we observed a decline in demand. Data so far in 2024 remains unfavorable; 10 positives, 17 negatives and two Flat print.

Weekly housing inventory data

The best story in 2024 is stock growth. It’s unlikely that we will have a fully functioning housing market at the level of inventory we will see in 2020-2023. We’ve gotten enough inventory growth this year to create a cushion so we don’t end up with another seriously unhealthy housing market when mortgage rates come down. I talked about this on CNBC recent.

For 2024, my model is simple: as interest rates increase, our weekly inventory growth should be 11,000 and 17,000 home. We’ve done this six times this year, last year it didn’t even happen once. We’re not quite at those levels yet as rates have dropped over the past two weeks, but the growth is enough to keep me smiling until the seasonal dip.

Inventory growth last week 6,482. I stress, we need this to have a normal housing market again!

- Weekly inventory changes (July 26-August 2): Inventory growth from 677,246 arrive 683,728

- Same week last year (July 27-August 3): Inventories rising 485,743 arrive 488,607

- Historical inventory bottom occurs in 2022 240,497

- Annual inventory peak in 2024 will occur this week 683,728

- For some purposes, active listings this week in 2015 were 1,195,876

New listing data

Another positive story is new listings data, a key variable in inventory growth this year. While I didn’t reach my minimum goal of 80,000 new listings during this year’s peak season, it’s good to see growth. The seasonal declines we are seeing now are very normal.

Here are the number of new listings last week over the past few years:

- 2024: 67,085

- 2023: 60,766

- 2022: 73,177

Price reduction percentage

On average, one in three homes loses price every year—standard housing activity. As mortgage rates remain high, price reduction percentages are higher than in the past two years and inventory in some parts of the country is higher than national data. Remember, as we adapt to workforce growth, we are working with demand at an all-time low.

A few weeks ago, I discussed on the HousingWire Daily podcast that price growth data would cool down in the second half of the year. Here are last week’s price reduction percentages over the past few years:

- 2024: 39%

- 2023: 35%

- 2022: 38%

for sale

Below is altos research corp. Weekly open contract data shows immediate demand compared with the same period last year. Our demand has increased this year as more sellers become buyers. Purchase app data tends to last 30-90 days, and the only time we see real growth in purchase app is in late 2022 and 2023, when rates dropped by more than 1%.

- 2024: 379,482

- 2023: 364,934

- 2022: 405,466

next week

It’s going to be a quiet week in terms of data, but Monday’s ISM and PMI reports, especially the services report, will be an interesting one. We’re going to have some bond auctions this week and Fed Chairman Barkin will be giving a speech. With the unemployment rate at 4.3%, all Fed chair speeches will now be watched more closely.