So where does this leave us? Let’s look at my labor economics model from April 7, 2020, and see where we are today.

1. The current situation in the labor market is the result of a series of events, of which COVID-19 was an important catalyst. I wrote the COVID-19 Recovery Model on April 7, 2020, and retired it on December 9, 2020.

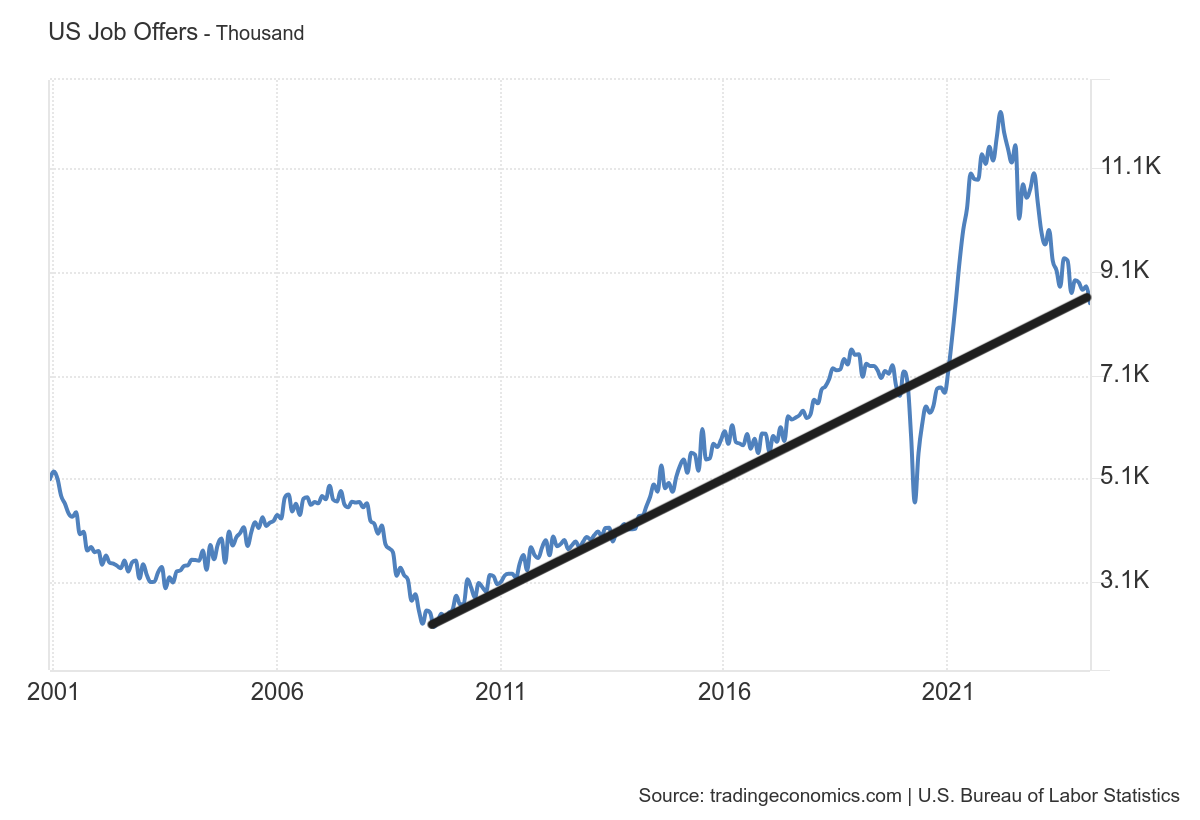

2. In the early stages of the labor market recovery, when we observe weak employment reports, I remain firmly convinced that there will be 10 million job openings in this recovery. Although the May 2021 jobs report was unexpected, I am confident in the trajectory of the recovery. Job vacancies once stood at 12 million and are now at 8.5 million. Today, the labor market is no longer tight, but the Fed would like to see that number lower, to 7 million.

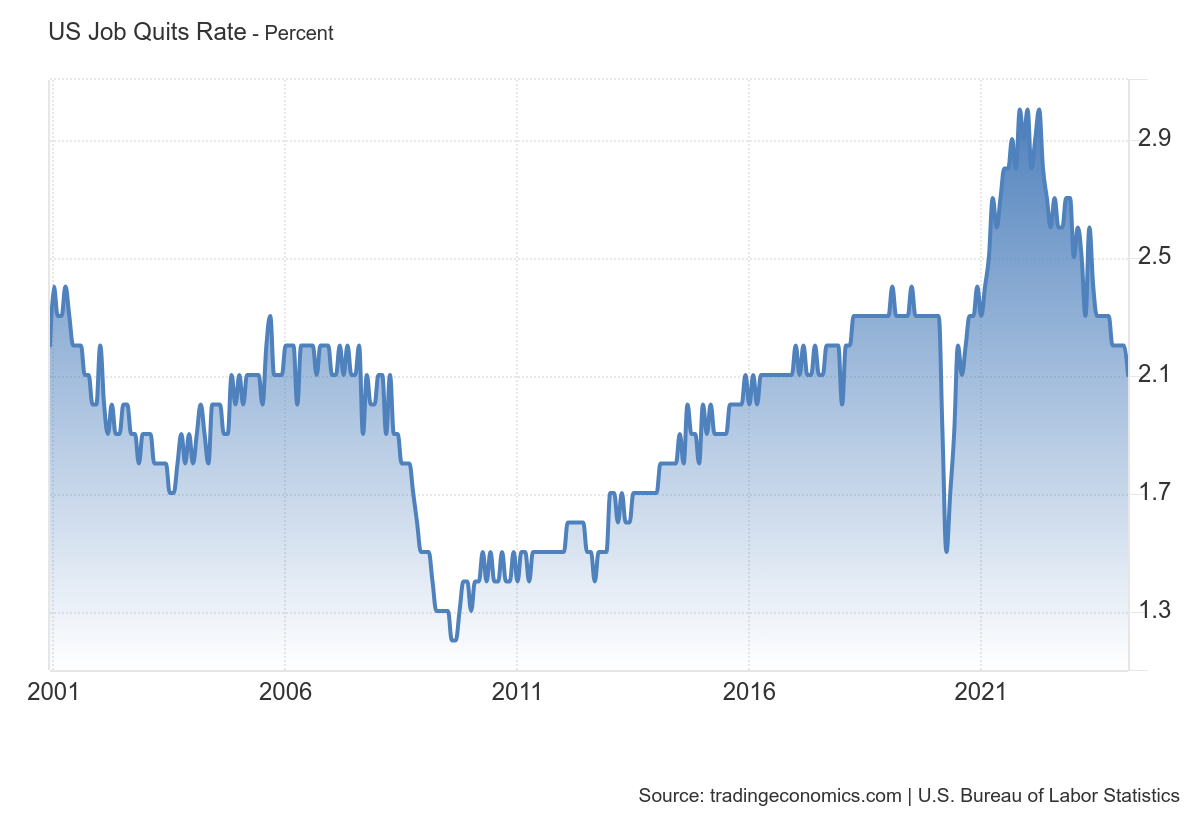

Currently, turnover and hiring data for open positions are below pre-COVID-19 levels. We’re getting closer to a single take on these numbers, and when they come from higher levels, that means any Fed member who talks about a tight labor market is sucking some good stuff.

3. I wrote that we should take back all the jobs lost to COVID-19 by September 2022.

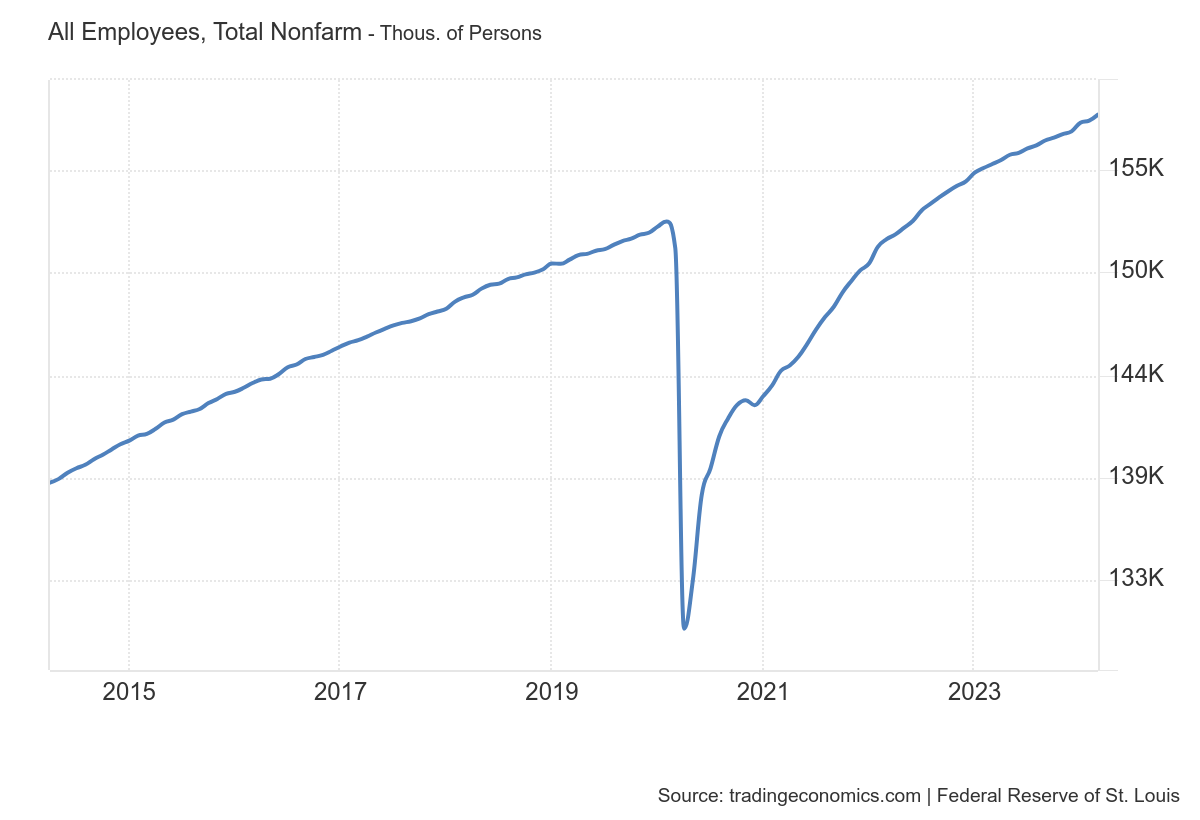

4. This is the key now: If COVID-19 had not happened, we would have between 157 million and 159 million jobs today, based on February 2020 job growth rates. This is crucial because given this level, employment growth should now be cooling.When the average number is 140,000 to 165,000, we will be more in line with what the labor market should be per month.

Today’s job printing 175,000 Still above my work target level, and we’re getting there 159 million Total non-agricultural employment population.I would be shocked if we were still trending higher than above 165,000 Once we break through, every month 159 The total number of employees is 10,000. That said, the labor market still performs better than my model.

Looking at the six-month average job growth data, we’re running 242,000, Even with all the modifications.I’m still above mine 165,000 per month level, but we are moving in that direction.

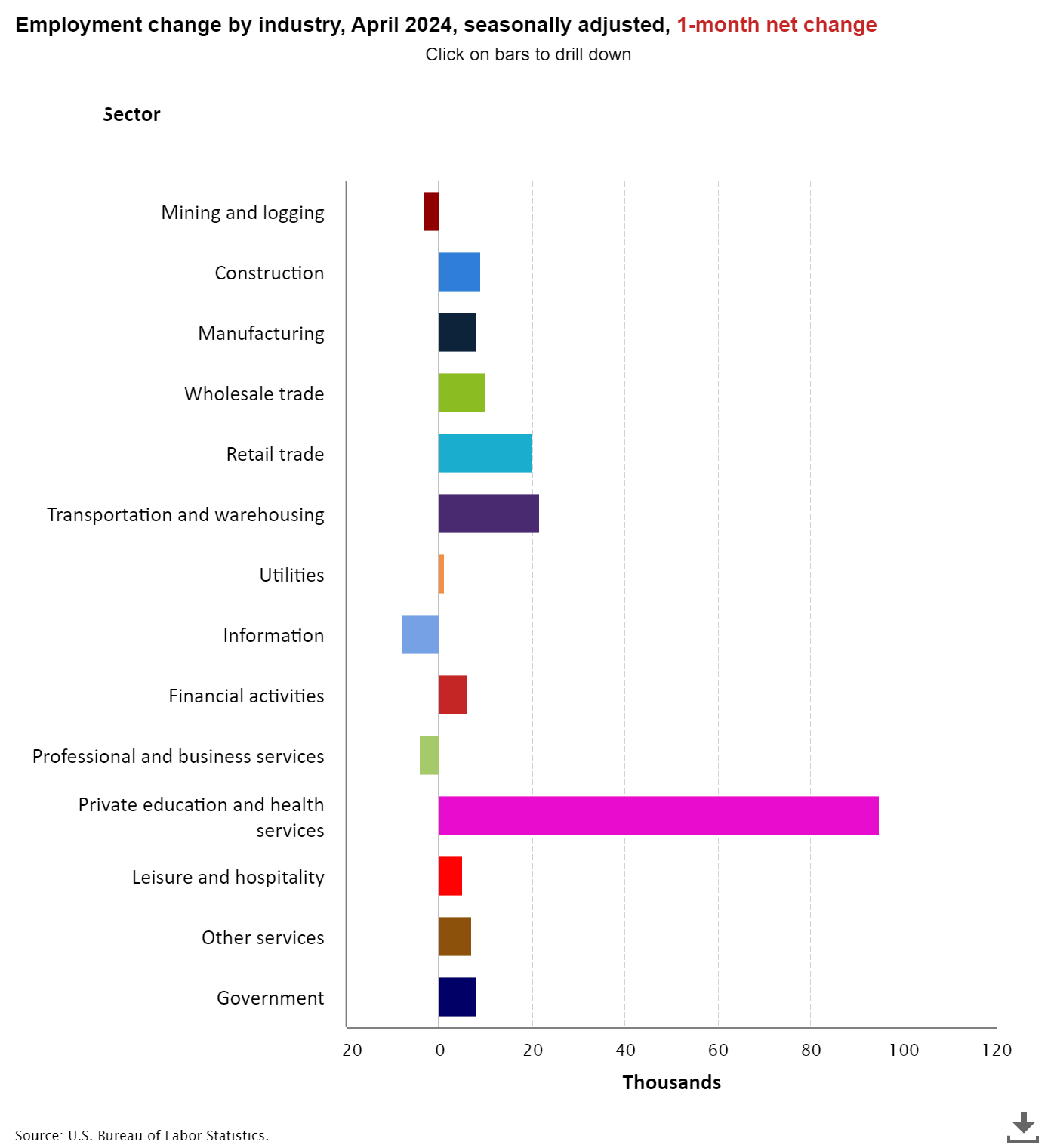

from Bureau of Labor Statistics: The U.S. Bureau of Labor Statistics reported today that nonfarm employment increased by 175,000 people in April and the unemployment rate was little changed at 3.9%.Job growth occurred in health care, social assistance, transportation and warehousing.

Here are the jobs created and lost last month:

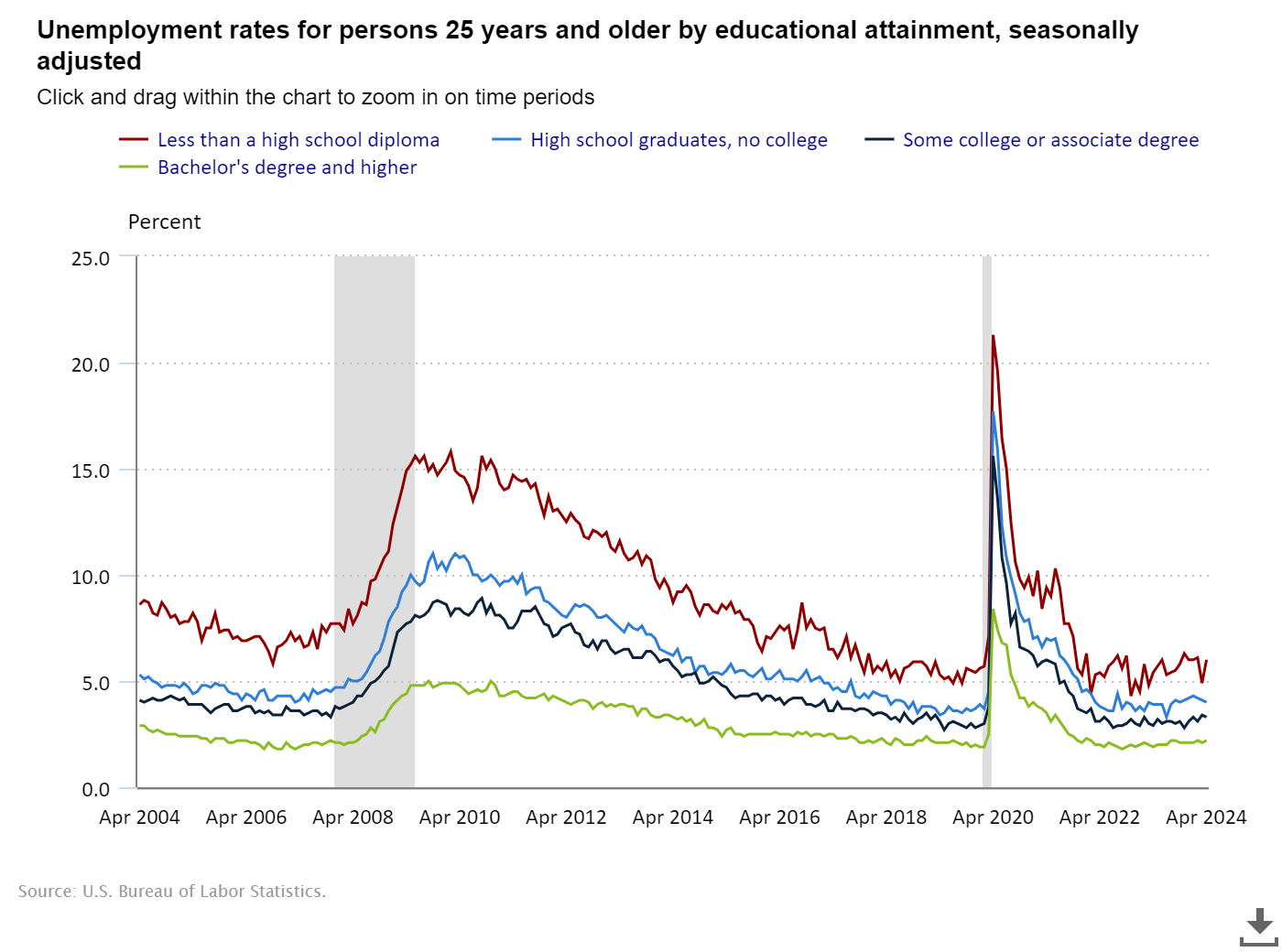

In this jobs report, the unemployment rates by education level are as follows:

- Less than a high school diploma: 6.0%

- High school graduate but no college: 4.0%

- Some College or Associate’s Degrees: 3.3%

- Bachelor degree or above: 2.2%

A key part of the report is that wage growth is slowing, which is key to many of the Fed’s concerns. The Fed likes 3% wage growth because they believe productivity is 1%. As shown below, wage growth continues to move in this direction.

We now have multiple data showing that the labor market is not as tight as it once was. The Fed is thinking about this now as they talk more about its dual mission as opposed to just being a single mission Fed. This is positive for mortgage rates because once mortgage rates turn around, we could see rates fall more consistently than we have to deal with from 2022 onwards. Growth is back down to the 3%-3.5% level, but at least it’s moving in that direction.